Intel Reports Q1 2015 Earnings: Lower PC Sales And Higher Data Center Revenues

by Brett Howse on April 14, 2015 11:00 PM EST- Posted in

- CPUs

- Intel

- Financial Results

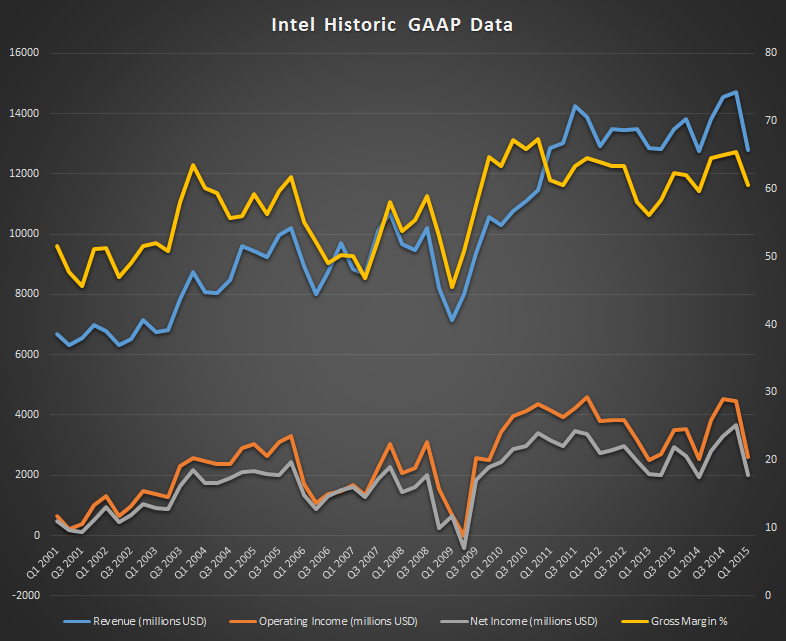

Intel released their Q1 2015 earnings today. The company posted revenues of $12.8 billion USD for the quarter which is down 13% from Q4 2014, and flat year-over-year. Gross Margin was 60.5%, which is up 0.9% over Q1 2014 and down 4.9% over last quarter. Operating Income came in at $2.6 billion, and Net Income was $2.0 billion, which was up 3% over Q1 2014 and down 46% as compared to their last quarter. Earnings per Share was $0.41, which is up 8% year-over-year and down 45% quarter-over-quarter.

There are a couple of notes to make about this year’s reporting structure. Last November it was made known that the Mobile division would merge with the PC Division. The Mobile division has long been a source of large operating losses mostly due to the contra revenue plan to boost Atom sales in tablets. It also should mean that mobile becomes as big of a priority for Intel as the PC CPU space, which should benefit the company in the long term with the push to lower power devices. For Q1 2015, Intel is no longer reporting the Mobile division as a separate reporting structure, and instead it will be combined into the Client Computing Group.

The new numbers will of course reflect this, so any year-over-year comparisons will also be compared with like-for-like data.

| Intel Q1 2015 Financial Results (GAAP) | |||||

| Q1'2015 | Q4'2014 | Q1'2014 | |||

| Revenue | $12.8B | $14.7B | $12.8B | ||

| Operating Income | $2.6B | $4.5B | $2.5B | ||

| Net Income | $2.0B | $3.7B | $1.9B | ||

| Gross Margin | 60.5% | 65.4% | 59.6% | ||

| Client Computing Group Revenue | $7.4B | -16% | -8% | ||

| Data Center Group Revenue | $3.7B | -10% | +19% | ||

| Internet of Things Revenue | $533M | -10% | +11% | ||

| Software and Services Revenue | $534M | -4% | -3% | ||

| All Other Revenue | $615M | 0% | +13% | ||

That being said, the Client Computing Group did not have an excellent quarter. Declining PC sales due to the slowing of corporate customers performing Windows 7 migrations has put a damper on this group. Revenue for the group was $7.4 billion, which is down 16% from last quarter, and down 8% from last year. Breaking the numbers down a bit further, desktop platform volumes were down 16% year-over-year, which is a pretty sharp decline. At the same time, the average selling price for desktop platforms went up 2% to help offset this loss. Notebook platforms on the other hand were up 3% year-over-year, but the average selling prices of notebook platforms went down 3%. Tablet volumes were up 45% as compared to Q1 2014. Compared to Q4 2014, the entire group had revenue down 16%, platform volumes down 18%, and average selling prices up 1%.

The Data Center Group had almost the polar opposite, with revenue of $3.7 billion which is up 19% year-over-year, with platform volumes up 15%, and average selling prices up 5%. Compared to Q4 2014, revenue was down 10% with volumes down 7% and average selling price also down 3%.

The Internet of Things group is still relatively small at Intel, but posted an 11% year-over-year growth with revenues now coming in at $533 million. This is a 10% drop as compared to Q4 2014.

Software and Services is roughly the same size of overall business as IoT, with revenues at $534 million, which was down 3% year-over-year and 4% quarter-over-quarter.

The “All Other” segment which includes non-volatile memory (NAND flash memory), SoCs for wearables and emerging computing, and corporate expenses had revenues of $615 million, up 13% year-over-year and flat quarter-over-quarter.

Intel bought back 26 million shares in Q1, meaning they have repurchased 203 million shares back since Q1 2014.

In Q2 we should start to see the new Atom chips come to market, and devices like the Surface 3 have already been confirmed to be running the latest 14 nm Atom chip. Also, there should be some talk of Skylake, which is the next Intel Core architecture, although details may be scarce until Q3.

On the financial side, Intel is forecasting revenue of $13.2 billion plus or minus $500 million for Q2, with a Gross Margin of 62%. For the full year, Intel is expecting revenue to remain flat.

Source: Intel

11 Comments

View All Comments

Mikemk - Wednesday, April 15, 2015 - link

To be expected when they only release low end/low power and server chips, and somehow keep forgetting mainstreamLaststop311 - Wednesday, April 15, 2015 - link

they aren't forgetting mainstream. Full power desktop PC's are on a sharp decline in popularity. With tablets and phones being good enough for all the minor low power stuff web browsing movie watching social networking etc and notebooks good enough for a lot of business and productivity stuff like excel and business inventory software and composing letters and answering business email and customer support etc and gaming notebooks for the most part more than sufficient for 1080p gaming with a 970m or higher, the percentage of population that requires a full powered desktop pc just keeps shrinking.So why is intel going to focus it's efforts on the full power desktop PC where it's all negative growth? The real money is in 45 watts and below cpu's and soc's. If intel can't start doing better with is sub 10watt tablet soc and sub 4 watt phone soc's they are going to be in trouble as more and more people start using only phones and tablets as their only PC's and even transition from using notebooks. Desktops are quickly becoming only used by content creators and the niche power gamers with the vast majority of regular folk having no need for that much power and favor the super portable solutions that do everything they need them to. Nowadays mainstream means gaming notebook or productivity focused ultrabook

Drumsticks - Wednesday, April 15, 2015 - link

It's extremely short sighted to think that Intel going mobile and low power ISN'T them targeting the mainstream.nathanddrews - Wednesday, April 15, 2015 - link

You said it yourself - that the loss-heavy Mobile Division has been merged with the PC Division. I'm not sure this is an accurate representation of the data.Shadowmaster625 - Wednesday, April 15, 2015 - link

Revenue flat for 4 years. Stock price up almost 100%. Good job Fed.Drumsticks - Wednesday, April 15, 2015 - link

"Details might be scare" in the second to last paragraph!Hrel - Wednesday, April 15, 2015 - link

Must be nice, to get away with having a monopoly to the point where you can consistently bring in a 60% profit margin.Kjella - Wednesday, April 15, 2015 - link

Gross margin only includes the direct costs - even AMD operates at a 35% gross margin. In practice you see Intel has 2.6/12.8 billion = 20% operating income to revenue (40% less), AMD is around zilch (35% less). So the way everyone else counts profits they're not all that profitable really.HollyDOL - Thursday, April 16, 2015 - link

It would seem reasonable to expect decline before release of next major cpu/chipset generation. My guess would be more or less half of that decline is just market starting to hold breath for next gen and/or better price on current one.blzd - Thursday, April 16, 2015 - link

Not surprising considering they only rebranded their desktop CPUs after a 100Mhz clock speed bump.It's just sad that I still bought one anyways, no other real choice and I didn't feel like waiting another 10 months.